How Much Does It Cost to Do a 1031 Exchange?

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

The cost of doing a 1031 exchange is a maze of IRS-qualified and non-qualified expenses. Some 1031 exchange fees paid out of sales proceeds will create taxable events. They include operating expenses such as prorated rents, security deposits, repairs and insurance premiums. Others, such as qualified Intermediary fees, broker commissions, and title closing fees are exempted.

We’ll delve into all this so you’ll know what expenses to anticipate and how to keep them down. You’ll be given options to avoid any threat to your exchange and now to limit or eliminate any taxable boot.

Qualified Intermediary Fees

Delayed 1031 Exchange Costs

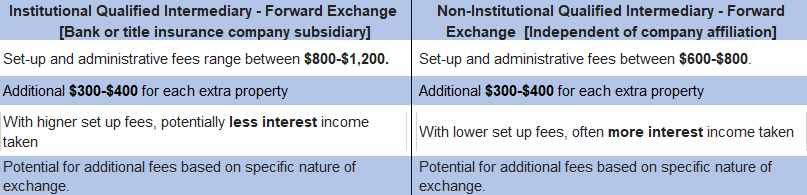

How much does it cost to prepare 1031 exchange documents? The 1031 exchange process starts with retaining a Qualified Intermediary (QI). You have a choice between either an institutional (bank or title company affiliated) or non-institutional (independent of company affiliation) 1031 exchange companies working in your area.

Non-institutional intermediaries tend to cost less. Average 1031 exchange facilitator fees to accommodate a Delayed Exchange range from $600-$800 for non-institutional and $800-$1,200 for institutional intermediaries.

This fee generally covers the qualifying, accommodation and administrative cost of completing a 1031 exchange. Included are messenger, document prep, statement, processing, and notary fees among other service costs.

Also, if you were to include additional properties to sell or acquire, the additional property fee could range from $300-$400.

Another significant factor is the opportunity cost when your QI keeps interest accrued on your escrowed funds. This can be material with 180 days lapsing from your relinquished property’s sale to the replacement’s closing. With net proceeds of $500,000 paying 2% interest, $5,000 in interest is accrued.

Rather than interest going to the QI, it could offset other expenses. But then expect the QI fee to be higher. It’s something to consider in selecting your QI and when drafting the contract. Just be sure to factor accrued interest into cost calculation.

Summarized here, special requirements unique to your exchange may result in additional fees.

For rush requests, the QI might pass on an overnight delivery charge if documents need to be sent quickly. Some QI’s will charge more based on the sales price of the properties, but most fees will fall into a broad dollar range.

More risk is assumed by QIs’ as exchange property values rise. As an offset, the amount of interest income accrued increases as property values escalate.

For example, you sell two properties for $500,000. One is an office building for $400,000 plus an adjoining parking garage for $100,000. After costs of the sale, mortgage payoffs, and other expenses, $300,000 is put in escrow.

You are trading up to a $800,000 office building. You’re charged a $1,000 set-up fee, $350 additional property fee, and $250 escrow fee with accrued interest returned to you. Your intermediary fee would total $1,600.

This example should give you insight into how to compare contract offers for a 1031 exchange facilitator. You should fully analyze and consider multiple factors. Many fees are not handled uniformly among exchanges.

Escrow fees e.g. may be included along with title insurance charges or billed separately. It’s your challenge to identify all non-qualified fees for payment outside of exchange funds should you want to avoid all boot.

This may be a good time to consider retaining outside tax advice. Getting answers to the following questions will help you make an informed decision.

- Does the QI require an exclusive contract?

- Is the QI a Federation of Exchange Accommodators (FEA) member?

- Has the QI provided credible references and a solid portfolio?

- Does the QI have expertise to match your specialized needs?

- How much are the set-up and administrative fees?

- How much extra are multiple properties assessed?

- Is the QI fidelity or surety bonded?

- Will funds be held in a Qualified Trust (QTA) or Qualified Escrow Account (QEA)?

- If so, what is the fee for a QTA or QEA?

- Who will retain accrued interest, and if you will, when will it be released?

- Will cash-out be released when available or not until 180 days have lapsed?

- How much are service charges such as wire transfers fees, check disbursement fees, et al?

- How much are rush charges for expedited rendering of services?

For better understanding of who a Qualified Intermediary is and how it’s different from a non-qualified intermediary, as well as to learn in more detail what they do for you in a 1031 transaction, read our article All About 1031 Exchange Accommodators (aka Facilitators or Qualified Intermediaries).

Reverse 1031 Exchange Costs

Expect to pay much more if you complete a Reverse or Construction 1031 exchange. As the name implies, in a Reverse Exchange you buy the replacement before selling your relinquished property.

Fees can be several times higher because of more complexities. It’s often employed in sellers’ markets where demands for properties are higher than available supplies. Not being constrained by the 45-day rule limiting the identification period of your 1031 exchange property may improve your chances of acquiring suitable replacement property.

Significantly there’s no interest income accrued with replacements purchased ahead of selling your old property. QIs will usually charge $3,000-$8,000 for a reverse exchange. That means more out of pocket cost but no foregone accrued interest.

Closing Costs

Can 1031 Exchange Funds Be Used for Closing Costs?

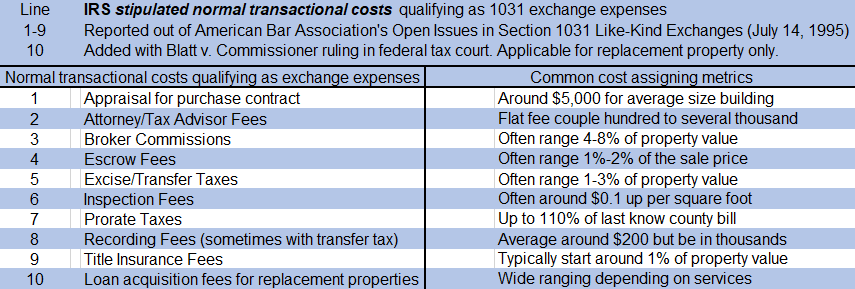

Yes, but the big question is which of these costs can be paid with exchange proceeds without producing a taxable event. The IRS stipulates only normal transactional costs qualify as 1031 exchange expenses.

For sure, a taxable boot is created if you take cash out of your 1031 exchange funds or do a partial 1031 exchange. Unfortunately, beyond that IRS regulations aren’t so conclusive. With significant ambiguity, you should be alert to problematic transactional expenses. Expenses customarily not paid at closing where the properties are located, should be paid out-of-pocket.

The American Bar Association in its Open Issues in Section 1031 Like-Kind Exchanges (July 14, 1995) report determined that the following list of nine costs meets IRS’ criteria.

Meanwhile the Tax Court in Blatt v. Commissioner ruled a replacement property loan cost was a qualified exchange expense. The distinction made was rather than being a typical cost of obtaining a new loan, it was for acquiring the property.

There are at least three important takeaways here.

- Intermediaries, attorneys and tax advisors are in general agreement over which costs qualify. However, each expense stands on its own merit with some requiring close examination. Even so, there could still be an IRS challenge.

- The big benefit of qualified exchange expenses is that they offset the gain realized from the relinquished property’s sale. Say you sell a property for $500,000 with qualified closing costs of $50,000. Your tax basis would be $450,000. Then the replacement property need only be $450,000 for full tax deferral. The closing costs effectively offset the gain realized on the sale. From a tax standpoint, the relinquished property effectively sold for $450,000.

- The list is not exhaustive. However, you and any advisor may infer from the nature of those items which additional costs may qualify. Similar to the Blatt case just cited, appraisals required by lenders, e.g. are loan acquisition not exchange expenses. But if a purchase or sales contract requirement exists, they are classified as exchange expenses. Section 1031 exchange facilitators, statements, processing, notary fees likely qualify, as well. Homeowner association assessments and repairs won’t qualify.

#1 Appraisal for purchase contract

Expect to pay $5,000 for an average size commercial property. Valuation of a large building may cost $10,000 or more. Note: appraisals for mortgage lenders don’t qualify.

#2 Attorney Fees

Attorneys and tax advisors usually charge flat fees ranging from a few hundred to several thousand dollars. They should set up the entire process and protect you from any adverse legal action. Then post-exchange, serve in a clean-up role, making sure no issues escape legal supervision. For a cost estimate, you may contact recommended commercial real estate lawyers in your area.

#3 Broker Commissions

Commissions vary depending on location, type, and size of property for sale. Real estate agents’ commission fees average between 5%-6% of properties final cost. Half goes to the seller agents and the rest to buyer agents.

#4 Escrow Fee

Escrow fees vary depending on which state you live in and what the escrow services are performed. Fees typically range between 1%-2% of the sale price.

Some escrow services set a base rate with additional fees added when more services are required during the escrow process.

#5 Excise/Transfer Taxes

Excise or transfer taxes are levied by most states and in some counties/cities with variations. Rates vary widely, but generally range between 1% and 3% of the exchange deal’s value.

Before selling a commercial property, the seller should check with the state and county for a tax estimate. The tax is usually due at the time of closing.

#6 Inspection Fees

A low-end inspection runs $0.1 per square foot on average. However, little commonality exists with commercial buildings so inspectors must improvise.

Lenders need to understand the condition of a property and whether there’s a significant amount of deferred maintenance. They’ll order a physical inspection to determine the amount of capital that is needed to fix up the property and ensure it’s safe, sturdy, and up to code. Costs will depend on size and type of asset. Usually within a wide range each type of office space has its own rate.

#7 Prorated Taxes

Sellers usually pay up to 110% of the latest real estate tax bill, prorated to the days owned at closing. The assumption is that the real estate taxes will have increased.

#8 Recording Fees

The national average for recording fees is under $200 but could exceed that by thousands of dollars in some jurisdictions.

Some states include recording fees with transfer taxes. States and counties around the US have different rules and regulations regarding the recording of deed transfers, liens, and mortgage recording.

In some locations, mortgage recording is a flat fee in the hundreds of dollars. Elsewhere, you may need to pay a percentage of the loan amount as a mortgage registration tax.

#9 Title Insurance Fees

All related title costs are typically set at 1% of the sales price. This includes:

- document preparation

- deed recording

- title insurance

- escrow fees.

Buyers usually pay for title insurance, included in the escrow paid by the buyer before the closing. It’s then deducted from the seller’s proceeds.

#10 Loan Acquisition Fees for Replacement Property

Loan acquisition costs involve replacement property services. These costs include origination fees and other fees related to acquiring the loan. It’s generally accepted that such costs may be paid from the proceeds of the loan.

Loan origination fees alone run around 0.5% of the amount you’re borrowing. This covers document preparation, notary, and lender attorney fees. Expect up to 1% of the loan in these acquisition fees.

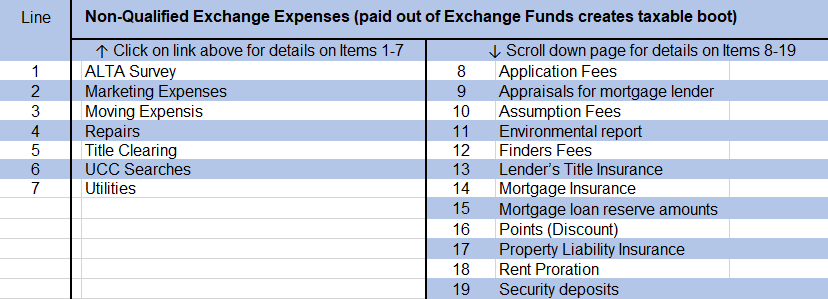

How are the Non-Qualified Exchanges Expenses Treated?

Consider what happens if you take $25,000 out of the exchange to pay non-qualified expenses. It’s a recognized capital gain subject to tax.

With a blended 30% tax rate, you’ll pay $7,500 in tax. Rather, paid with $25,000 in outside funds, you’ll preserve $25,000 in exchange funds and tax deferrals. The $7,500 gains tax liability will be avoided, as well.

Many tax advisors endorse that approach, recommending non-qualified fees be paid in advance of the closing altogether. Barring that, you may pay directly out-of-pocket at closing.

That’s why bringing cash to the closing when possible is also recommended. You’ll be meeting important investor objectives. More exchange funds left on the table for additional investments or less debt in replacement properties.

Other non-exchange expenses listed below would be treated as usual on any sale closing, i.e. expensed or capitalized as applicable. See our guide on commercial real estate closing costs for details on Items 1-7 listed below and scroll down for Items 8-19.

#8 Application Fees

A fee likely around $100 charged by the lender when submitting your application.

#9 Appraisals for Mortgage Lenders

Lenders need to verify the amount you request for a loan is justified and make sure it can recoup the value of the property on any loan default. The average cost for commercial property appraisals by certified professional appraisers ranges from $450-$650. It varies depending on the property size and loan type. Paid directly to the appraiser, it’s nonrefundable on completion of the appraisal.

#10 Assumption Fees

If you assume a mortgage on a property, an assumption fee is the charge paid by the mortgage holder. Typically, you’ve bought property that hasn’t been paid off yet. Still the original seller retains secondary liability except when released by the buyer. The assumption fee can’t exceed 1% existing loan balance at closing.

#11 Environmental Report

A physical review of buildings and land for any environmental problems are required steps on your commercial property due diligence checklist for obtaining financing. A qualified engineer would also review historical documents and other land-use records.

If your property passes this Phase I environmental review, the added expense of a Phase II remediation is avoided. While costs range widely, a $3,000 Phase I estimate is reasonable.

If not, as a buyer your contract must include the right to undertake a Phase II environmental assessment. If problems are uncovered, you must have the option to either require the seller to resolve them to your satisfaction or to back out of the deal.

There’s even more uncertainty regarding Phase II costs. They could range from a few thousands to much more, e.g. if serious contamination exists.

#12 Finders Fees

Often called a referral fee, it’s essentially a commission paid to a middleman. These fees are non-obligatory commissions paid to facilitators of transactions. They discover deals and bring together parties. Many states allow an intermediary asking fee to be from 3%-35% of the total value of the deal. Services provided range from locating a property with certain specifications for a client to closing a deal.

#13 Lender’s Title Insurance

This protects your lender should title issues arise. The cost is set by the state based upon the policy size. Typically, it’s 0.5% of the purchase price.

#14 Mortgage Protection Insurance

Upfront mortgage insurance premiums are paid at the time of closing. It protects the lender from losses if you were to default on the loan. Rates may range from 1%-2% of the loan amount.

#15 Mortgage Loan Reserve Amounts

Considered emergency funds, they are your savings balances left after closing. Lenders may require your liquid reserves be equal to several months or a year’s worth of loan payments. You’d multiply your monthly loan payment times the number of months specified by the lender to calculate the reserve requirement.

The following qualify as liquid reserves: checking or savings accounts; stock or bond investments; certificates of deposit; trust accounts; 401k, IRA, or other retirement savings account; and vested life insurance policy cash value.

#16 Points

Points are optional fees paid to lenders to reduce your interest rate charged for a mortgage loan. Each closing point equals 1% of the total loan amount. Also known as discount points or mortgage points, they’re paid at closing of the mortgage transaction.

#17 Property Liability Insurance

Lenders require some level of insurance to protect against natural disasters such as floods, earthquakes, environmental hazards, et al. As a commercial loan, your premium would be based on the project’s ability to earn income, not on your credit history. That might involve a comprehensive study of the project. A range of $500-$2,000 annually would cover most situations.

#18 Rent Proration & #19 Security Deposits

Often sellers holding security and prorated rent deposits will credit them against the sale price. If the seller is doing a 1031 exchange, it’s important to understand how those credits will affect the seller’s exchange.

Say you’re selling a property for $500,000 while holding $10,000 in prorated rents and security deposits. Disregarding other costs, you would reduce your asking price to $490,000.

1031 Exchange Costs – Summary

How to Minimize Your 1031 Exchange Expenses?

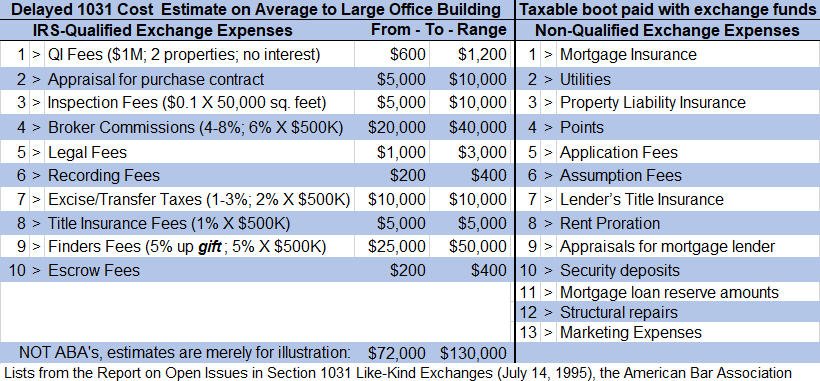

Yes, the cost of doing a 1031 exchange is high. Note though that the lion’s share of these costs

are:

- broker commission

- appraisal fee

- finders fee

- taxes

- title fees.

In any event, you’d expect to pay those expenses in any real estate sale or purchase. The onetime Qualified Intermediary fee seems quite manageable, starting under $1,000 for a single property Delayed Exchange.

A key consideration is identifying expenses payable with exchange funds from non-qualifying ones. Tax advisors generally recommend paying non-qualified expenses out of pocket. Avoiding taxable boot meets your 1031 objective of defer taxes with this exchange.

After all, tax deferrals could reach into the thousands of dollars and beyond. Finally, we shouldn’t lose sight of the overarching goal to acquire great replacement properties at fair prices.

A reputable Qualified Intermediary will help you and your tax advisor/CPA plan your 1031 exchange expenses. The professionals at the 1031 exchange company will consult you on what costs you can or can not avoid in your particular situation to perfectly comply with the IRS rules and get the most benefit of the transaction.

PropertyCashin is an all-in-one platform for commercial real estate investors that maintains relationships with top-rated 1031 exchange firms in all locations of the USA. To get connected with the best professionals and have your exchange processed safely and effectively, fill out the form below.