Step-by-Step 1031 Exchange Process and Timelines Explained

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

We’ll walk you through the ever-popular Forward (Delayed) and Reverse 1031 Exchanges. The same timeline applies to both exchanges. Only the sale/purchase ordering of relinquished (old) and replacement (new) property is reversed.

Many of the same benefits also apply to both exchanges. They preserve your equity by deferring capital gains and other taxes. Both allow you to expand, diversify, and relocate your investment properties tax-free. These are among the many solid reasons to consider tax-deferred 1031 exchanges.

You’ll gain a good understanding here of what it takes to complete both most popular types of 1031 exchanges.

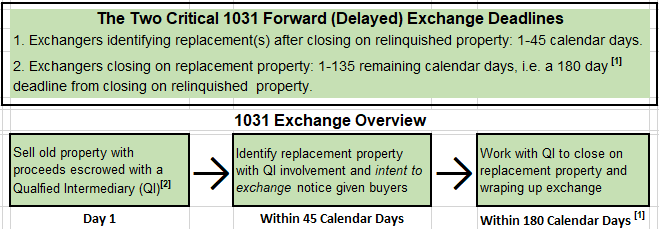

Timeline for a Forward 1031 Exchange

There are two important 1031 exchange dates to consider in this exchange timeline:

- the lapse time allowed to identify replacement(s) after closing on your relinquished property

- the replacement(s) closing date.

[1] Caveat: IRS rules require your exchange be reported on that year’s income tax return. That could be an issue should your exchange start late in the year. Not to cut short your 180-day deadline, you may need to file a return extension. Usually you’re precluded from amending later, which would result in a taxable transaction.

[2] When considering a 1031 Delayed Exchange on selling your investment property, a Qualified Intermediary (QI) is generally required. The QI prepares the necessary documentation for holding your exchange funds and processing your replacement property’s acquisition. You can choose one from our directory featuring the best 1031 exchange companies in your local area.

Note: the process is somewhat simpler if exchanging a real property into trust shares or acquiring interest in tenants in common property. For more information, read our guides:

- Can You Do a 1031 Exchange into a REIT with Section 721 Exchange?

- Delaware Statutory Trust (DST) 1031 Exchange Explained

- Tenants in Common (TIC) 1031 Exchanges

6-Step 1031 Exchange Process and Deadlines for Forward (Delayed) Exchanges

Step 1: Plan Your Exchange

First things first: you should have a solid rationale for doing an exchange. Have you weighed tax deferral and any other benefits against 1031’s costs and sometimes-arduous requirements? Maybe you’d like to exchange low income-producing properties or relocate your investments. Then, a tax-deferred 1031 exchange might make perfect sense.

Or perhaps it makes more sense to sell multiple properties with one exchange? Section 1031 exchange deadlines make orchestrating such an exchange a bigger challenge. The timeline countdown starts when the first of the several sales closes. Both the 45-day and 180-day deadlines revert back to that first closing.

Also, with multiple sales grouped into one exchange, identifying replacements is limited to only:

- three properties of unlimited value or

- more than three properties whose combined values do not exceed 200% of the value of properties being sold.

You must decide whether one multiple property exchange or several separate exchanges is best. More separate exchanges provide greater flexibility with renewed timelines with each one. Then again it may not be practical to be buying replacements under separate purchase agreements.

A partial 1031 exchange is also possible albeit more complicated. There’s no requirement that you exchange 100% of the property. You’ll need to make sure the exchange documents properly reflect included amounts in percentage terms.

In any event, unless you’re a pro at this, discussions with a tax advisor are advisable. You’ll need a realistic strategy that avoids pitfalls. Well-conceived planning is invaluable, especially considering those ever-looming deadlines.

Step 2: Retain a Qualified Intermediary (QI)

As a safe-harbor, retain a QI or a 1031 exchange facilitator to take your place as the relinquished property or properties seller.

Warning: your receipt (actual or constructive) of sale proceeds at this point likely rules out a successful 1031 exchange. IRS Section 1.1031(k)-1(g)(6) provides that you can’t receive, pledge, or borrow against these funds.

Adhering to QI procedures will eliminate this and other potential problems. Ideally engage your QI at least one week prior to the closing. Enter an Exchange Agreement assigning to your QI:

- seller’s rights for the relinquished property or properties and

- buyer’s rights for the replacement(s).

This must be done before the relinquished property’s or properties’ closing date. Your QI then acts on your behalf to establish an escrowed exchange fund to receive sale proceeds.

Replacement(s) will be acquired later using these same funds. Post-closing, the QI provides you with an escrow account statement and lays out the 45 and 180 calendar-day timeline for completing the exchange.

As is evident here, working with a competent QI is essential to a smooth, error-free exchange. Getting credible answers to the following questions will help you make an informed selection.

Is the QI

- unqualified as a family member, employee, financial connection, or your agent?

- holding an Employer Identification (FIN) Number?

- requiring an exclusive contract?

- a Federation of Exchange Accommodators (FEA) member?

- providing credible references and a solid portfolio?

- an expert in areas matching your specialized needs?

- offering fixed set-up and administrative fees?

- charging extra for multiple properties assessed?

- fidelity or surety bonded?

- having funds held in a Qualified Trust (QTA) or Qualified Escrow Account (QEA)?

- charging a QTA or QEA fee?

- retaining accrued interest as QI income, but if not when will it be released to you?

- releasing any cash-out immediately or not until 180 days have lapsed?

- charging fees for such services as wire transfers fees, check disbursement fees, rush charges for expedited rendering of services, et al?

The next step is identifying replacement property or properties, unless you have already closed on replacement property within the first 45 calendar days. If you want to learn more about property identification requirements, we have an entire guide on the 45 day period rule and other 1031 exchange property identification rules.

Step 3: Listing Your Property for Sale

After retaining a QI, your next step is corralling a buyer. Retain an experienced realtor/broker to market your relinquished property or properties. They’ll be listed for sale as usual except for giving notice of your 1031 exchange intent. Potential buyers are put on notice that they’ll need to work within 1031 constraints. Fortunately, that entails little more than sign off on assignments and disclosures.

Step 4: Negotiate and Close on Your Relinquished Property or Properties Sale

A title company or attorney handles the closing, almost per usual. Only now the intermediary gets involved with sale proceeds transferred to the QI’s bank account, not yours.

Note: When a buyer is found, they’ve already received notice that 1031 compliance is needed. Nevertheless, many experts recommend adding a special sales agreement clause. It simply confirms that the buyer intends to cooperate on the exchange. It’s a safeguard since the buyer must comply with your 1031 exchange to succeed.

Step 5: Identify up to Three Replacement Properties Within 45 Days

You must identify potential replacement property(ies) within 45 calendar days of the relinquished property or properties closing. A legal description or property address has to be presented in writing.

Within that 45-days you may however change identified properties at will. Just revoke the previous ones and identify new potential replacements.

For multiple properties, one of the following three rules applies. Identify:

- up to three properties of any fair market value (FMV), intending to purchase at least one,

- more than three properties having a total FMV not exceeding 200% of the relinquished property’s or properties’ FMV, or

- more than three properties having a total FMV not exceeding 200% of the relinquished property’s or properties’ FMV, knowing that 95% of the FMV of all properties identified must be acquired.

Another Caveat: When choosing replacement(s) don’t create unintended taxable boot (learn more about boot from our article How Is Boot Taxed in a 1031 Exchange?). The following choices trigger at least partial loss of tax deferrals. They include:

- withdrawing cash from sale proceeds

- paying less than the replacement(s) exchange value[3]

- not replacing debt paid off on relinquished property or properties with new debt or cash

- obtaining a larger replacement(s) mortgage than being carried on relinquished property or properties, and

- paying debt unsecured by a mortgage or deed of trust.

[3] Replacement closing costs are added to determine exchange value. Loan fees and prorations don’t reduce the exchange value of replacements.

Step 6: Negotiate and Accept a Purchase Offer

Finally, have your QI reach a sale agreement with your replacement property seller. You, any agent, and your QI work together with the title company or closing attorney.

All details of the process must be concluded and your replacement’s title received within the shorter of 180 days or that tax year’s filing deadline. Non-compliance with this and the 45 day deadline is not an option!

Direct the QI to enter into a Purchase & Sale Agreement (PSA) with that seller. This Agreement should include language similar to that contained in your relinquished property or properties agreement.

Make sure the seller is aware that it’s a 1031 exchange purchase. In accordance with the Exchange Agreement, your QI will use your relinquished property proceeds to purchase the replacement(s).

Then transfer your proceeds over to the title company or attorney. The property closes as in a regular transaction. After receiving payment, the property is deeded over to you. You’ll receive title to your replacement property.

Note: If you’ve made multiple offers, you could also go under contract on all three of your identified properties. Using contingency clauses, you could terminate offers you later decide not to pursue.

Common Mistakes when Doing a Delayed 1031 Exchange

With a successful exchange, any capital gains taxes you might have incurred are deferred. They’ll only be due in the future, if ever. Remember that 1031 exchanges play on. You can repeat this same exchange endlessly. And continue deferring taxes indefinitely.

This helps build wealth over time. When otherwise you could be paying over 30% in gains, any state, and other taxes. Any added Alternative Minimum Tax (AMT) and depreciation recapture are avoided. All the while enhancing your property investment portfolio.

Just be sure not to make common mistakes such as:

- missing deadlines

- forgetting 1031 exchange deadlines such as the 180 days might be cut short without an extended federal tax return due date

- not knowing paying less than the replacement(s) exchange value creates boot

- not adding cash or new debt should replacement(s) mortgage be less than relinquished property’s or properties’ debt

- not starting your replacement search before the exchange clock starts running[3]

- not ensuring your QI escrows your sales proceeds in a separate FDIC account

- making closing errors exposing you to capital gains, depreciation recapture, state, and alternative minimum taxes

- failing one of your highest exchange priorities, not choosing a highly competent QI.

[3] If running out of time searching for suitable replacement(s) is a concern, reverse exchanges covered next may be right for you.

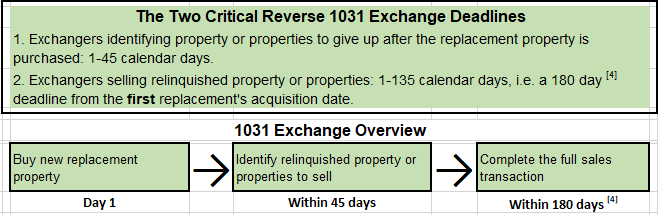

Reverse 1031 Exchange Process and Timeline

The Reverse timeline is unchanged from a Forward Exchange except the selling/buying of properties is reversed. Here you first purchase replacement(s) before selling relinquished property or properties.

All transactions must be completed within 180 calendar days of the initial purchase(s).[4] But the clock only starts after you’ve acquired replacement(s).

[4] Caveat: IRS rules require your exchange be reported on that year’s income tax return. That could be an issue should your exchange start late in the year. Not to cut short your 180th day deadline, you may need to file an extension. Usually you’re precluded from amending later, which will result in a taxable transaction.

8-Step Reverse 1031 Exchange Process and Deadlines

Variances from Forward (Delayed) 1031 Exchanges

A reverse 1031 exchange permits you to purchase more replacement(s) before selling your relinquished property or properties. Here you’ll need deep pockets to purchase new property or properties upfront without relinquished property proceeds.

There are two ways for completing reverse exchanges: the exchange last (most popular) or the exchange first reverse.

- With an exchange last reverse, the Exchange Accommodator Titleholder (EAT to be defined) holds title to replacement(s) until your relinquished property or properties are sold.

- For an exchange first reverse, investors buy replacement(s) directly through a lender while the EAT receives the titles. Here you will need deep pockets to purchase new property or properties upfront.

Rule one is you must be both the buyer and seller of all properties.

Step 1: Retain a Qualified Intermediary (QI)

We recommend this be your first step in the exchange process. The QI guides you throughout including Step 2, i.e. creating an Exchange Accommodator Titleholder (EAT).

Altogether QIs are go-between the buyers, sellers, IRS, and you. They

- prepare 1031 exchange agreements including the Purchase and Sales Agreement (PSA); qualified exchange accommodation arrangement (QEAA); promissory note; and replacement leases

- transfer titles of the relinquished properties to new buyers

- acquire titles to parked replacements

- receive buyer funds for acquisition of parked properties from your Exchange Accommodator Titleholder (EAT).

Finally, a QI’s main duty is to transfer both properties’ title from the EAT to respective owners. Learn more about them in our guide All About 1031 Exchange Accommodators (aka Facilitators or Qualified Intermediaries).

Step 2: Create an Exchange Accommodator Titleholder (EAT)

In reverse 1031 exchanges, you can’t hold title to both new and old properties at the same time. An Exchange Accommodator Titleholder (EAT) is created.

A qualified exchange accommodation arrangement (QEAA) is reached between you and the EAT. The EAT will hold, i.e. park [5] or take title to one of the properties per the agreement.

If relinquished property’s or properties’ sale proceeds exceed the QI amount needed to acquire parked replacement(s), you may identify additional replacements.

It must be done within 45 days of transferring relinquished properties. And again, all transactions must be completed within 180 days of transfers.

[5] EATs most often acquire and then park legal title to replacement(s).

- You or 3rd party lenders provide funds for EATs to purchase and title replacements.

- EATs may temporarily lease back replacements to you. This allows you to use replacement(s) while being held by EATs. Typically, a triple net lease along with rent, you must pay all related expenses including taxes, building insurance, and maintenance.

- When you sell identified relinquished property or properties, titles are transferred directly to buyers via direct deeding.

- Sale proceeds are received by the QI to acquire replacement(s) from the EAT.

- EATs first repay the loan from you and then 3rd party replacement(s) debt holders.

Finally, parked replacement(s) titles are transferred to you.

Step 3: Find Replacement Property

You may buy with cash or with loans. Lenders and title companies must be informed that you’re planning a reverse 1031 exchange. Be mindful that once a replacement is purchased, you have 45 calendar days to identify up to three properties to sell (relinquish).

Note: To avoid taxable boot, replacement(s) must be equal to or greater in value than the relinquished property or properties.

Step 4: Sign a Purchase and Sales Agreement (PSA)

The seller and you sign PSAs for the replacement(s). Again, PSAs should alert sellers to your exchange intent. Also be sure to alert title companies of your reverse 1031 exchange intentions.

Of course, you can’t hold title to replacement(s) just yet. The title must instead be held by an Exchange Accommodation Titleholder (EAT) to hold onto, or park, the title throughout the 1031 exchange process for tax purposes.

Now you have to decide on one of two reverse variations.

- With exchange last reverse 1031 exchanges, EATs acquire replacement(s) and holds/parks them pending sale of your relinquished property or properties. In this regard, be sure your contract permits title transfers to your chosen EAT. While these reverses are preferred by most pros, concerns are raised among some lenders. They’re apprehensive about EATs holding title to replacement(s). You or your tax advisor may want to flesh this out with prospective lenders. With exchange last reverses, be sure your contract permits title transfers to your chosen EAT.

- With exchange first reverse 1031 exchanges, you acquire your replacement(s) first. You transfer the title to the EAT at the same time you receive lender loans. This requires reinvesting all your relinquished property equity in your replacement(s) before closing on the relinquished property or properties sale. This means having cash on hand for replacement(s) before receiving relinquished properties’ proceeds.

Step 5: Prepare Closing Documents on Replacement(s)

Again, this is usually done by the QI. Documents include title insurance reports and escrow instructions to inspection reports and proof of insurance. The intermediary might also ask you to provide additional documentation for commercial real estate due diligence and pre-transaction screening.

Step 6: Identify Property or Properties to Be Sold

You have 45 days from the replacement(s) purchase date to identify relinquished property or properties. Then, you’ll have another 135 days (180 days from the exchange outset) to complete the sale.

Should relinquished property be parked, replacement(s) don’t need to be identified. If replacement(s) are parked, relinquished property or properties are identified as for sale.

Step 7: Enter into PSA with Relinquished Property Buyer

You sign a Purchase and Sales Agreement (PSA) with the buyer of the relinquished property or properties that includes 1031 assignment language.

Again, PSAs are used in complex transactions to convey terms and conditions of the investment. You agree to relinquish ownership of the relinquished property or properties.

Step 8: Final Closing Documents and Agreements Are Signed

When parked relinquished properties are sold, your QI

- receives purchase funds from buyers

- transfers proceeds to you or replacement(s) lender

- acquires all property and respective titles from the EAT

- transfers parked relinquished properties with titles to buyers

- transfers replacement(s) with title to you.

Title to replacement(s) must be conveyed to you no later than the 180th day after closing on the first replacement.

Pros and Cons of Reverse 1031 Exchanges

A Reverse 1031 exchange is a tax deferral strategy that’s inviting you to first buy. Take your time finding the most suitable replacement(s). Then sell your relinquished properties.

In a Forward exchange, you cannot change your mind after 45 days. Should Identified properties go off the market or you’re out-bid by other buyers, your exchange fails.

Lost are all the tax and other 1031 exchange benefits. Reverse 1031 exchanges eliminate a lot of those stresses. Along with usual savings through tax deferral and new property investment opportunities generated, that’s the good news.

Above all, you need the financial wherewithal to purchase replacement property. Some commercial lenders won’t lend to an EAT. As well, there are almost always more costs associated with reverse exchanges. Given the higher risk involved, EATs may charge around $7,000 and QI’s $3,500. A standard exchange might cost under $1,000.

What happens when a reverse exchange fails? Often real estate company holding agreements provide for the transfer of whatever property it’s holding to you at the end of 180 days. In the end, you own both relinquished and replacement properties. And of course, there’s no tax deferral.

With the sometimes-arduous process just described, it’s clear you’ll need a full understanding of Reverse exchanges to safely proceed. It’s a big investment decision, so be sure to plan well ahead.

Revisit the previous section’s Forward (Delayed) 1031 Exchange Checklist for the same mistakes to avoid in a reverse exchange. Exploit the many resources available for assistance and consult with a tax advisor.

How to Comply with All IRS Rules

Unless you are doing a simultaneous 1031 exchange, you must use a Qualified Intermediary. Professional QIs are experts in all aspects of 1031 exchanges.

A reputable 1031 exchange company with tax attorneys on their team will consult you and your tax advisor/CPA and guide you through each step of the 1031 exchange process. Before the exchange, they will review your situation and advise on whether your plans satisfy the IRS requirements or need adjustments to perfectly comply with the rules.

PropertyCashin is an all-in-one platform for commercial real estate investors that maintains relationships with top-rated 1031 exchange firms in all locations of the USA. To get connected with the best professionals and have your exchange processed safely and effectively, fill out the form below.