9 Ways to Avoid or Minimize Capital Gains Tax (CGT) on Commercial Investment Property in 2024

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

From this guide you will learn how to avoid paying capital gains tax (CGT) when selling your commercial investment property either fully or partially. In the USA, there are 9 ways and instruments to do it legally:

- deducting capital losses

- long-term investments

- qualified opportunity zones

- 1031 Tax-deferred exchange

- 1033 Tax-deferred exchange

- 721 Tax-deferred exchange

- Section 453: Installment Sale Tax Deferral

- tax-advantaged retirement plans

- charitable remainder trusts.

Note: you might also be interested in our guides on commercial real estate property tax:

- ABC’s of Commercial and Industrial Real Estate Property Taxation

- 5 Robust Commercial Property Tax Reduction Methods

Now, let’s start with the most obvious method of reducing your capital gains tax obligations.

9 Ways to Avoid or Minimize Capital Gains Tax (CGT) on Commercial Real Estate

#1 Deduct Capital Losses

Simply put, a capital loss occurs when the property is sold at a loss — for less than the price you had acquired it for plus the cost of improvements. By using the capital losses, you can reduce (offset) the capital gains tax basis.

Let’s take a simplified example: you sold one property at a loss, and in the same year you got capital gains on the sale of another one. You may reduce the taxable amount of the capital gains from the sale of the second property by deducting the loss from the sale of the first property from it.

Generally speaking, at the end of the tax year you should net all capital gains on all of your taxable assets sold during the year. You should also net all capital losses. Then, the losses should be deducted from the gains.

Note: for a better understanding of how capital gains tax works and what other kinds of taxes apply when selling commercial real estate, read our guide Tax Implications of Selling Commercial Investment Property.

Yes, complexities come with computing loss amounts and determining when and where they apply. Typically, both the investment’s purchase price and selling price must be adjusted. Only then will reported capital gains and losses fly with the IRS and the Courts.

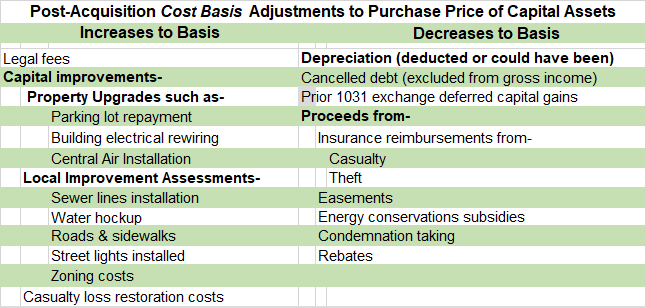

Tax Basis Adjustments

Tax or cost basis adjustments to an investment’s purchase price are critical to maximizing deductible losses. The chart below lists some adjusting expenses and proceeds that impact the purchase price. Left-column costs listed below grow capital losses while right column depreciation and proceeds shrink losses.

Sales Price Adjustments

Likewise, calculating realized capital gains/losses requires adjustments to sales price. Selling costs are subtracted. Such costs include advertising and legal fees, sales commissions and bank fees paid by you, the seller. When there’s a loss, of course, reducing the sales price increases it.

How Capital Losses Offset Capital Gains

Typically, not a happy event, capital losses may nonetheless be put to good use. Until exhausted, capital losses offset capital gains in the year gains are realized. That’s a big deal! For example: In 2016, your $40,000 capital loss offsets a $14,000 capital gain — along with the standard $3,000 annual deduction against ordinary income ($40,00 minus $17,000 = $23,000 remaining loss).

With no capital gains the following two years, $6,000 offsets ordinary income, leaving a $17,000 loss carryforward. In 2019, $10,000 in capital gains and $3,000 in ordinary income are offset. Now you still have $4,000 in capital losses ($17,000 minus $13,000) left for future use, while having excluded $36,000 from taxation, including $24,000 in capital gains.

This translates into big tax saving, somewhere around $10,000. How much depends on your filing status (Single, Head of Household, or Joint filers) and total taxable income reported. For long-term capital gains, 20% tops the tax bracket while for short-term it’s 37%, which is also the top ordinary income tax rate.

Don’t leave money on the table! Fully utilize those nearly inevitable losses investors incur.

When You Can Not Apply a Capital Loss

Let’s not get ahead of ourselves! To qualify for favorable treatment as capital losses, commercial investment properties must be held for investment, not for business or personal use. Clearly, they can’t be Section 179 depreciable assets destined for write-off.

If you intend to qualify them, take appropriate steps from the start. No do overs later — they should support investment intent. Ultimately, you control the facts and circumstances which will prevail should any transaction be contested.

At sale, how well can you answer this question: for what purpose was the property being held when sold? You say investment, but will the IRS and the Courts agree? Maybe not, e.g., if you purchased land and sold subdivide parcels. Courts have declared proceeds from such sales as ordinary income. At the same time, Courts have qualified undivided land sales. In that regard, building-out infrastructure (streets, et al) is indicative of dealer and not investor activity.

Real estate may be subdivided before purchase, preventing any one parcel’s unfavorable outcome from tainting others. Another factor: at the outset, sales agreements, investor letters and other documents should clearly and accurately reflect holdings’ intent.

Courts have also heavily weighted purchases and sales frequency? Low sales volume coupled with high profit margins suggests real estate is being held as an investment. Another important component is marketing. If all it entailed was a listing of properties for sale versus advertising, customer solicitations, et al, once again the dealer tag will likely stick.

If you’re uncertain about any of these considerations, seek professional tax counsel before acting. Some actions (and inactions) are irreversible. With the many proactive tax savings measures available, missteps are costly.

Lots to consider with possibly lots at stake.

#2 Long-Term Investment

Gains on the sale of commercial real estate property owned for more than one year are classified as long-term. Such properties may qualify for significant capital gains tax benefits. An important qualifier: assets must have been held for investment and not business purposes when sold. See the When You Can Not Apply a Capital Loss section for details.

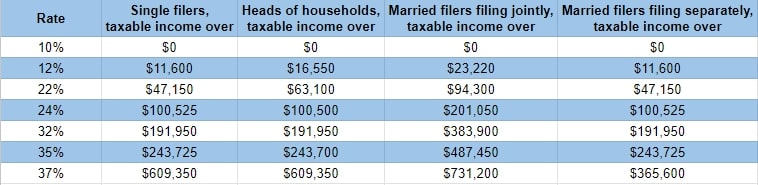

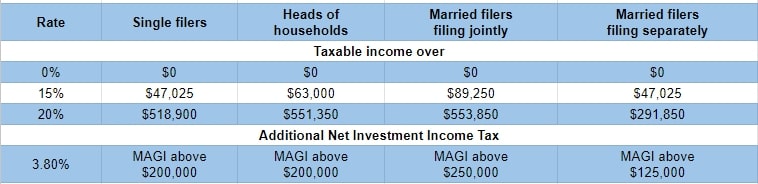

If qualified, real estate sale profits are taxed at long-term gains rates (chart below) starting at $40,000 applied at 0%, 15% or 20% rates depending upon taxable income and filing status. Conversely, short-term rates start at under $10,000 and top out at 37%. See the Capital Loss section above for adjusting purchase and sale price details necessary to compute capital gains (profits). Computing gains — but not hardly the tax — is the same for both long- and short-term investment holding periods.

Compare tax rates on the two tables below. What a difference a day can make! No brainer it would seem unless there’s a compelling reason to sell your commercial property fast. Are you holding any big gainers and sure losers?

Let’s return to the example in the Capital Loss section above. Let’s say that the $14,000 gain was a must sell in 2016 while the $40,000 capital loss came from a long-held sure loser. Timing is often key to smart investing. Maybe 2016 was the best year to offset realized capital gains with that stinker? It keeps giving, too, until exhausted by the $3,000 annual reduction to ordinary tax income. Or you sell another capital gains winner.

Do the math with a calendar by your side.

Long Term Capital Gain Tax Brackets and Rates for 2024

Short Term Capital Gain Tax Brackets and Rates for 2024

#3 Qualified Opportunity Zones

Selected by state governors in 2018, Qualified Opportunity Zones (QOZs) were created in all fifty states and six territories to revitalize economically distressed communities.

To make money here, investors must first generate capital gains by selling qualified property for a profit. The goal then becomes capital gains tax avoidance. Form 8896 is filed with the IRS to create a Fund, structured either as a partnership or corporation. Then at least 90% of the Fund investment is held in that qualified Zone’s property — including real estate, with limitations.

Buildings must be newly constructed or major upgrades made to existing ones. Other restrictions require all construction to be completed within 30 months of purchase. Existing building improvement costs must equal the building’s purchase price.

Lots of red tape! It’s due to the program’s intent: growing targeted communities economically. Nonetheless, big tax reduction incentives often make it worthwhile, such as:

- allowing income taxes on reinvested capital gains proceeds to be deferred up to the end of 2026

- reducing taxes on Zone capital gains by 10% when investments are held at least five years as of December 31, 2026 (15% if held seven years up to year-end 2026)

- excluding from CGT taxation altogether profits from Fund investments held at least ten years

- avoiding the opportunity zone depreciation recapture tax altogether when held at least 10 years.

Quite an impressive list of tax incentives, not just deferrals but permanent tax avoidance opportunities here!

#4 1031 Tax-Deferred Exchange

Four exchange types share this space, but the 1031 exchange dominates. Many of its rules apply to the other three types (explained further in this guide) as well. In like-kind property exchanges, investors defer paying capital gains, depreciation recapture, and income taxes on commercial investment property when it’s sold.

“Like-kind” doesn’t mean exact. Replacement commercial properties held for investment will qualify for exchange if relinquished properties were similarly investment properties. For example, you can exchange an apartment building for land.

To qualify — once again the “investment vs. business” caveat applies (covered earlier in this guide under the When You Can Not Apply a Capital Loss section). All properties must be held as investments. Inventory held in your real estate business as a flipper, e.g., doesn’t qualify for a §1031 exchange. In addition, the same investor must hold title to both the relinquished and replacement properties.

Generally, these exchanges allow you to keep all your money invested rather than losing equity to taxes usually in the 20-30% range! There are exceptions. If all proceeds from the relinquished property aren’t reinvested, investors pay capital gains tax on the cash boot. If replacement properties have debt lower than those relinquished, investors pay capital gains tax on the so-called mortgage boot. That tax is avoided if equivalent cash is added to the purchase price.

Most often these exchanges are delayed (Starker or forward exchanges), requiring sale proceeds be held by a qualified intermediary (QI) until reinvested in another property. Within 45 days of a relinquished property’s closing, qualified replacement properties (often up to three possibilities recommended) are identified. Closing must then follow within 135 days (180 days total) for completion of the exchange.

Three other types of §1031 exchanges are listed here.

- Reverse exchanges occur when replacement property is acquired before the relinquished property is sold. This “you buy first, and exchange later” exchange requires cash, which many banks won’t loan (but hard money lenders will). Also, an exchange is forfeited if the relinquished property isn’t sold within the required 180 days.

- Construction or improvement exchanges allow investors to use deferred tax dollars (equity) to improve replacement property being held by a qualified intermediary. Before titles are returned — within 180 days — all equity must be spent on improvements.

- Simultaneous exchanges occur when replacement and relinquished properties are exchanged on the same day. Investors swap each other’s properties at the same closing, no qualified intermediary required.

If you are interested in this way of tax deferral, you may want to look at our directory listing the best 1031 exchange companies providing qualified intermediary services in your location.

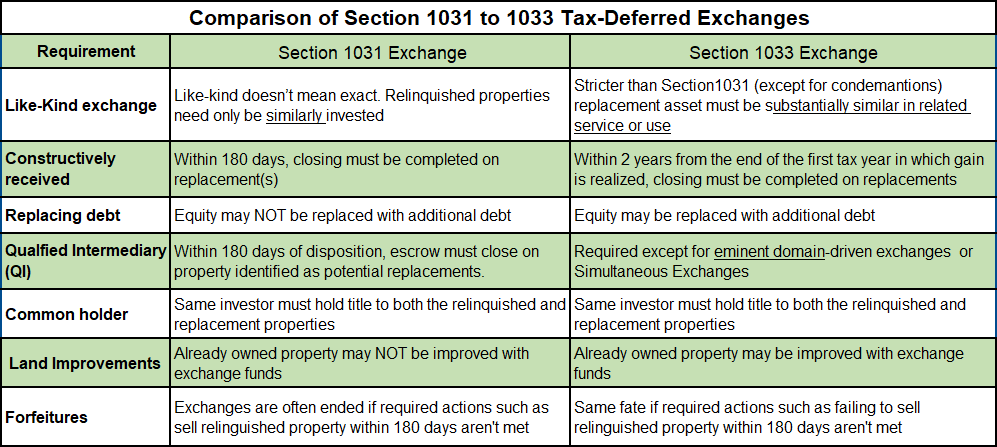

#5 1033 Tax-Deferred Exchange

With Section 1031 similarities, realized gain from an involuntary conversion (e.g., loss to casualty or condemnation) can be deferred if the owner acquires like-kind replacement property. The same investor must hold title to both the relinquished and replacement properties. Casualty-related direct conversions qualify when the replacement properties are substantially similar in related service or use. Condemnation-related indirect conversions must be like-kind akin to §1031 exchanges.

Qualifying replacement property costs must be equal to or greater than the amounts realized on conversions. Unlike §1031, equity may be replaced with additional debt. Debt may be replaced with additional equity (cash). If less than the replacement cost, gain recognition applies to the underinvested portion. Related-party acquisitions may also trigger gain recognition.

Generally, casualty lost property must be replaced within two years of the loss year. Replacements for eminent domain losses have a three years limit. Further, insurance proceeds need not be held until the replacement property is acquired and no qualified intermediary (QI) is required.

The chart below compares the main requirements of §1031 with §1033.

#6 Section 721 Tax-Deferred Exchange

A §721 Exchange or UPREIT allows investors to exchange investment property for Real Estate Investment Trust (REIT) shares or an Operating Partnership. No replacement property is required, and sale proceeds may be held by REITs pre-closing.

§721 and §1031 exchanges may be combined. Often, investors will hold §1031 exchanges sponsored by REITs for two years. Then with investment consolidation, holders will receive direct ownership of REIT shares. This conversion triggers no capital gains or depreciation recapture taxation. However, you can’t exchange out of REITs and have tax deferred.

Shareholders are passive investors uninvolved in managing REIT holdings. As with §1031 and §1033 exchanges, investors’ goals typically include tax deferral, diversification, and estate planning. REITs do:

- offer diversification benefit often with disperse property locations and wide range of industries and asset classifications

- provide real estate appreciation and dividend income

- disarm potential inheritance conflict over division of property

- provide heirs step-up basis while avoiding all taxes deferred by the estate.

Clearly, these are complex tax arrangements requiring professional guidance before acting. Nonetheless, tax savings and wealth-building opportunities outlined here are too great not to explore!

#7 Section 453: Installment Sale Tax Deferral

A specific §453 Installment Sales may be used to defer capital gains taxes by breaking up payments over multiple installments. A third-party deferred sales trust will reinvest your capital while indefinitely deferring your capital gains tax obligation.

Deferred Sales Trusts provide a means to defer capital gains on your appreciated property sales. It is an alternative to §1031, 1033 or 721 exchanges. Instead of buyers paying you in full for your property, they agree to make periodic installments. You may then realize gains over time or even defer them indefinitely.

Your recognition of capital gains starts with receipt of the first installment. You start by calculating a gross profit ratio based upon what the capital gains tax would have been on an outright sale. That ratio is applied to installments as received to determine what portion is subject to capital gains tax annually.

In the example below, $150,000 represents taxable capital gains recognized annually over the four-year predetermined payout period. With a $1M sale (contract) price reduced by a $400,000 adjusted cost basis (detailed in the #1 Capital Loss chart) for $600,000 gross profit. A gross profit ratio of 0.60 is produced by dividing that gain by the $1M sale price. Applied to the annual $250,000 installment, the taxable gain is $150,000 annually over four years.

That’s the basics. It’ll get more complicated with selling expenses, mortgage debt, and any other adjustments. Selling expenses decreases the gross profit ratio while adding qualified debt increases the ratio.

While this method defers taxes (four years in above illustration), capital gains may also be deferred indefinitely. Let’s say your property — transferred to a third party — is then sold to acquire a REIT. Covered here under a Section 721 Tax Deferred Exchange, the REIT makes regular distributions to contributors. If you receive periodic installments from this sale’s proceeds only — none from the original sale — no capital gains are realized.

However, receiving any profit ($600,000 in the above example) from the original sale will incur a capital gains tax obligation. Also, any depreciation recapture must be recognized in the disposition year.

#8 Tax-Advantaged Retirement Plans

Unlike Roth’s, you can defer capital gains taxes up to allowable limits with traditional IRA or 401(k) contributions. They’re among a short list of retirement plans classified as follows.

- IRAs and 401(k) — as an employee, all income and gains will generally flow back to your 401(k) plan without tax. However, low contribution thresholds limit its value.

- SEP-IRA (Simplified Employee Pension Individual Retirement Arrangements) — in addition to your own 401(k) — as a freelancer — this plan provides retirement benefits for you and any employees. Funds are invested the same way as most other IRAs. A similar Solo 401(k) plan may be opted for instead.

- Roth IRA — you can’t defer capital gains from current-year taxes. Taxes are paid upfront under this plan, which makes distributions on retirement tax-free. Nice when even in retirement taxes are pinching your lifestyle.

- Standard Brokerage Account — there are no special tax breaks here, but investing versus saving has historically paid big dividends.

A word to the wise. Retirement plans max-out quickly for high earners. Making retirement contributions in a specific order is key to maximize savings. As many as you can, consider saving to a:

- 401(k) first up to any employer match (that free money)

- traditional IRA or Roth up to the annual limit

- SEP-IRA if available for more earnings per-tax

- standard brokerage account, any discretionary funds.

#9 Charitable Remainder Trusts

Appreciated assets may be transferred to Charitable Remainder Trusts (CRT) tax free for a specific term. Contributions are irrevocable but grantors may have some control over them, even switching to another qualified charity. Since CRTs are tax-exempt, the trustee (you, the grantor) may sell contributed assets, thereby allowing proceeds to compound tax free.

Collateral benefits include removing assets from estate taxation. At the same time, you’ll be receiving distributions (generally taxable) annually from one of the following four types of trusts.

1. Charitable lead annuity trusts pay a fixed amount annually to designed charities.

2. Charitable lead unitrusts pay a fixed percentage of the trust’s value annually to designated charities.

3. Charitable remainder annuity trusts pay a fixed amount annually to grantors.

4. Charitable remainder unitrusts pay a fixed percentage of the trust’s value annually to grantors.

As an income beneficiary, formulating a tax strategy is complex. Income is reported first as generated from trusts, then unrealized capital gains, and finally return of capital. Factors unique to each beneficiary — from charitable intent to tax bracket concerns — make planning a challenge best left to pros.

Is There Any Capital Gain Exemption on the Sale of a Commercial Property?

To be precise, there’s no exemption pe se from capital gains taxation on commercial real estate. Ok — if you’re selling a home you’ve lived in for two of the past five years, you can exempt up to $250,000 in capital gains from taxation and $500,000 if you’re married. Not commercial real estate or residential rental property.

Avoid, minimize, defer—sure! First, be sure you’re dealing with property that meets IRS’ capital asset definition. If qualified, there are many tax-saving opportunities available to real estate investors explained above.

In general, these approaches don’t forgive taxes. Rather they provide workarounds for tax avoidance, minimization, or deferral. Timely implemented without defect, they frequently result in big savings. Sometimes huge savings — by most any standard — and occasionally even forgiveness. Not up to acting on every last tax saving opportunity. Then, retaining a tax professional may be money wise.