Ultimate Industrial and Commercial Property Taxation Guide

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

From this guide you will learn about the basics of industrial and commercial property taxation. We will discuss:

- who and how determines your commercial property tax rate

- what influences this rate

- what you can do to reduce your property tax due.

Now, let’s start with the definition of the commercial real estate tax.

How Commercial and Industrial Property Taxation Works in the U.S.

What is the nature of taxation on commercial property? Is there a difference between real estate and property taxes? Not interchangeable, real estate taxes are levied on real, immovable property only, while the term property taxes is all-inclusive with tangible personal property (cars, boats, et al) a major component. Just real estate taxes will be covered here.

Also, do not confuse real estate tax with capital gains tax on selling your investment real estate property that we covered in another article as well as commercial property capital gains tax reduction methods.

Commercial real estate tax paid by owners of commercial property is an ad valorem tax on land, buildings, and other structures. Latin for according to value, ad valorem taxes are levied on commercial real estate based upon assessed value.

First, what are these properties exactly? Municipal governments typically designate three basic real estate property types, namely commercial, industrial, and residential.

- Commercial properties include those used exclusively by the owner for business purposes. Commercial buildings include apartment buildings, office buildings, restaurants, arcades, shopping malls, parking lots, storage units, and bars.These properties are usually located in areas zoned for businesses having direct contact with their customers. It’s where consumer-facing businesses typically operate.Commercial real estate may be subdivided into classes for grading purposes. Real estate tax assessors, as well as investors and realtors use these ratings to evaluate property values. While there’s no official standard, the Building Owners and Managers Association (BOMA) assigns office space an A, B, or C classification.Subclasses from A+ down to C- are subsequently added. A+ properties are judged to have the best construction, location, security, parking, and access. Older, poorly maintained properties might fall to C- in blighted areas.

- Industrial property includes factories, warehouses, industrial parks, mines, and farms. Buildings may be used for manufacturing, assembly, research, storage, and distribution centers. These properties are usually larger in size and many locations include access to transportation hubs such as trucking depots, rail lines and harbors.

- Residential are those properties not classified as either commercial or industrial property. They are generally owner-occupied single-family houses.

How Is Commercial Real Estate Tax Determined?

Taxation on commercial property is within the purview of local municipalities. Jurisdictions such as counties, cities, and school districts (hereafter, municipalities) – independent of each other – levy the tax. Many rules and processes are unique statewide to each taxing authority. You’ll need to understand them to make an informed judgment on your tax bill’s fairness.

While there’s no universal approach, commonalities do exist on how the tax is determined.

- Municipalities hire (occasionally elect) assessors, sometimes called appraisers. They determine a property’s value upon which an established tax rate (also called mill rate) is applied. They may be overseen by an assessment board. For example, Bucks County Pennsylvania Board’s duties are described on the County’s website as follows:The primary function of the Board of Assessments Appeals is to determine the CURRENT MARKET VALUE of all properties in the County and calculate the appropriate assessment. The Board, which is composed of three members, has administrative duties which are strictly governed under Statutes established by the General Assembly for the Commonwealth of Pennsylvania. The Board maintains policies, manages operations, and supervises the assessments within the County.Note, nothing is said about setting tax (mill) rates. Who does it will be covered later.

- An equalization multiplier (EAV) may be applied to normalize valuations between different geographic areas. In an area deemed underassessed, e.g., a 1.25 multiplier applied to an existing $100,000 valuation would result in a new $125,000 assessed value. This EAV is the revised value used to calculate property taxes.

- Frequently, commercial property tax rates are expressed as mill rates. One mill is equal to $1 in property tax levied per $1,000 of assessed value. For example, assessed value (say $4M) must be divided by $1,000 to first calculate the number of $1,000 units. Dividing $1,000 into $4,000,000 equals 4,000 units. Then multiply 4,000 times the $8 mill rate for $32,000 tax due. You’ll also see this example as part of a Cap Rate chart displayed later.

With variations, most often assessors use one of the following three ways to calculate assessed value. That value times the mill rate determines your tax. We explained these three ways in more detail in our article about commercial property appraisal methods. But let’s make a quick overview of each.

Sales Method

For recent, comparable sales at fair market value (FMV), these prices would be the assessor’s starting point for calculating assessed value. FMV is a reasonable price willing sellers and buyers – both without constraints – could agree upon. Every office building, mall, land tract, other property might be revalued based on the current real estate trends. A timely example is the ongoing pandemic and civil unrest, which could impact the market and ultimately tax revenues.

Factors inflating valuations include land improvements, property access to public water and sewer, and prime locations for development. These are some of the same factors considered when properties are graded from A+ to C- as described in the section above.

Cost Method

Assessors estimate costs of building a similar structure on the same land to determine assessed value. That’s followed by would-have-been depreciation being calculated to reach the current valuation. More specifically, the estimate usually involves one of two methods. Replacement assumes near replication using modern construction methods and materials. Reproduction assumes duplicating property, materials, and design.

Then, structures and improvements are depreciated. Any economic downturn or other negative development also decreases estimated costs. Additions include the FMV of comparable vacant land.

Income Method

Each assessment period, the municipality has property owners submit an income and expense form* to its assessment office. To summarize the chart below, an assessor starts by computing a Capitalization (Cap) Rate by dividing (say $500,000) Net Operating Income (NOI) by current value ($5,000,000) taken from recent comparable sales. That equals a 0.1 or 10% cap rate, which in turn is divided into Net Profit of $400,000 for an Assessed Value of $4,000,000. The $4M is divided by $1,000 equals 4,000 against which to multiply the mill rate. At $8 per $1,000 mill rate, tax due is $32,000.

List ALL arguably valid deductions. Allow the assessor to propose any adjustments.

As with the other two approaches (Sales and Cost methods), any overstatement of current FMV value inflates assessed value and tax due!

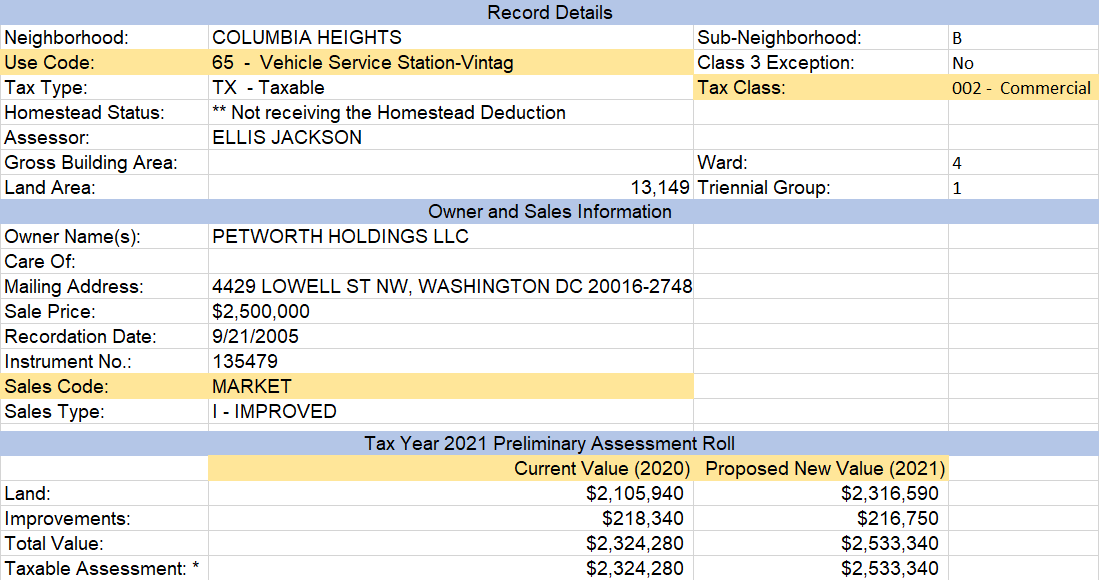

Property value data are compiled into an assessment roll, a master list of real property valuations in the municipality. It is a public record such as this District of Columbia example.

Rolls contain assessed property values and related information. Note the Use classification (vehicle Service Station); Tax Class 002 – Commercial (explanation coming up); Current Value (2020); and Proposed New Valve (2021).

Also, a previous sale is listed as MARKET suggesting the listed $2.5M sale price represented fair market value (FMV) when sold. FMV is a reasonable price willing sellers and buyers – both without constraints – could agree upon. It’s a critical Sales Method component for evaluations.

Who Determines My Real Estate Tax?

Assessors (appraisers) calculate assessed values following a prescribed methodology, likely one of the three approaches just described. They don’t set tax rates, establish special rules, deductions and credits, or determine other tax-related policies.

Rather, follow the money to identify your commercial and industrial property tax deciders. Legislators, or whoever set state and local budgets, dictate how much tax you pay by setting mill rates. Often these deciders are elected officials acting on budget needed or voter demands. They may hold public hearings for input on proposed rates.

Next up is how the tax (mill) rate is calculated.

How Is the Real Estate Tax Rate Calculated?

Many municipalities statewide determine how much money is needed to pay for services covered by taxation on commercial and industrial property. They rely heavily on this tax to fund education, parks and recreation, transportation, utilities, sewer, and other infrastructure, emergency services, et al.

- The tax is levied against properties within a city, county, school district, or other boundary.

- With each jurisdiction’s tax rate computed separately, all levies are combined for a composite tax (mill) rate for entire regions.

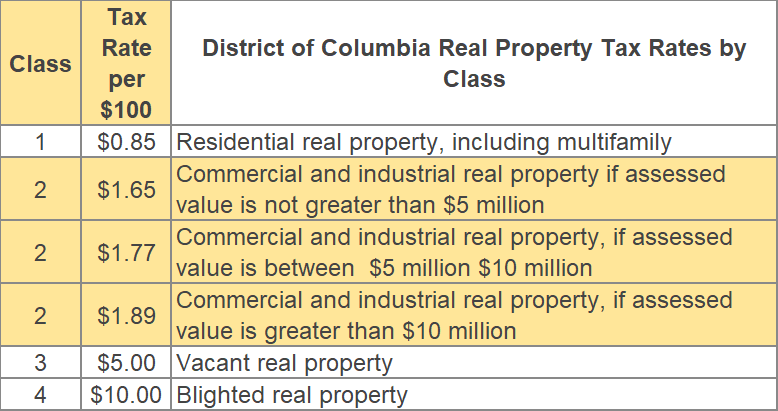

For example, say all budgetary needs call for $1M in revenues (tax receipts) and assessed values total $100M for the region. The required average tax rate would be $1M divided by $100M or 1% (the mill rate is then $1 per $1,000 assessed value). It’s an average rate because mill rates may differ within classes such as illustrated below. Note another quirk. The District’s mill rate is per $100 rather than $1,000. Still other municipalities use percentages.

This is what assessors have to work with. They must apportion the tax burden according to the value of all included properties. We’ve covered the three ways assessors usually use to calculate assessed value. How it’s a matter of multiplying property’s value times tax rate(s).

Bottom line $100M in total assessed values times mill rate(s) needs to produce the budgeted $1M in tax receipt.

In summary, with budgets in hand, municipalities set mill rates after they receive assessor-provided total assessed values for the region. Budgeted revenues are divided by total assessed values to produce mill rates. A real estate tax bill is the product of that rate times the assessed value of each taxpayer’s commercial or industrial holdings.

What Are the Commercial Property Tax Reduction Methods?

There are five common ways that professional property tax consultants use to legally reduce their clients’ property tax:

- commercial property tax deductions

- avoiding installment payment fees

- using early payment benefits

- cost segregation studies

- property tax appeals

If you want to learn more about them, we have an entire guide dedicated to reducing your commercial real estate property tax.

And if you are interested in being connected with reputable property tax consultants in your area, fill out the form below. As a national all-in-one platform for commercial real estate investors, we manage relationships with the top-rated tax consulting and appeal companies in each U.S. state and Washington D.C. After receiving your submission, we will review it and connect you with the best local specialist who can help you.