Can You Do a 1031 Exchange and Avoid Depreciation Recapture?

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

Section 1031 Exchanges are all about deferring taxes in asset sales. While deferring capital gains taxes often grab the headlines, depreciation recapture costs can skyrocket as well.

Tax deferral for both taxes is dependent upon a successful 1031 exchange. Depreciation recapture deferrals are however somewhat more nuanced than gains.

With you as the exchanger, we’ll outline how depreciation recapture is calculated and deferred in a 1031 Exchange. In the end, we’ll also show how both of these taxes can eventually be avoided altogether.

What Is Depreciation Recapture?

Complex rules are involved when depreciable (§1250) real estate is sold. Depreciation recapture is realized when an asset’s adjusted sales price exceeds its adjusted cost (tax) basis.

Simply stated: on sale a portion of depreciated properties’ gain will be denied favorable capital gains treatment. That’s because a portion of that gain is the result of prior depreciation being deducted annually.

Each year prior to the sale, depreciation was (or should have been) expensed to reduce taxable income. Depreciation recapture excludes that accumulated depreciation expense from favorable capital gains treatment. The intent is to preclude double-dipping, i.e. denying a second tax break.

In reality the asset hadn’t actually depreciated in value. It sold for more than the purchase price. So that tax-saving depreciation portion of the gain will now be taxed as ordinary income capped at 25% rather than the standard 37% top rate.

With your first successful 1031 Exchange, you’ll defer both taxes. Effectively, you create an IRS I Owe You (IOU) to which any subsequent tax deferrals can be added. A failed 1031 exchange will recall that IOU. Capital gains and depreciation recapture taxes will be imposed. Failed exchanges often happen if the exchanger doesn’t meet the 45 day 1031 exchange property identification period rule or other requirements.

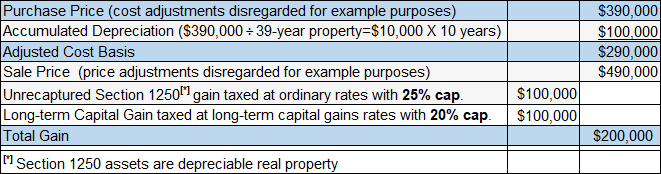

After 10 years, e.g., you sell a 39-year rental property costing $390,000 for $490,000. Over those years, you’ve expensed (or should have) $100,000 in depreciation. The property now has an adjusted cost basis of $290,000. Your gain is $200,000 ($490,000 minus $290,000).

The $100,000 §1250 portion of the gain is depreciation being recaptured and excluded from favorable long-term capital gains tax rates.

Not that complicated yet but there’s more to consider in computing depreciation recapture taxes.

What Happens when the Replacement Is of Less Value than the Relinquished Property?

Say in the 1031 exchange process you exchanged your debt-free relinquished property of $490,000 value.

- With an adjusted basis of $294,000 you have a $200,000 capital gain.

- Your replacement has a $390,000 debt-free basis.

- Having exchanged your $490,000 property for a $394,000 asset, $100,000 of 1031 exchange cash boot is taxable at ordinary income tax rates.

- Still those taxes on the remaining $100,000 can be deferred, i.e. the $200,000 gain from the relinquished property sale minus $100,000 taxable boot.

It’s a similar situation to a partial 1031 exchange when an investor exchanges only part of the relinquished property’s value (normally a larger one) and cashes out on the rest. You may also be interested in reading our article Can I Take Cash Out of My 1031 Exchange?

What Happens with Debt-Burdened Properties?

Let’s say that property sells for $490,000 with a $90,000 mortgage balance.

- Replacement property is acquired for $490,000 with a $40,000 mortgage. The replacement’s net value is $450,000 versus $400,000 for relinquished property.

- Effectively, you as the exchanger have an additional $50,000 gain. An additional $50,000 ($90,000 minus $40,000) is mortgage boot subject to tax at ordinary income tax rates.

You may also be interested in a related article: Can I Refinance a 1031 Exchange Property?

How to Compute Taxes Due

Let’s go over calculating tax due when:

- capital gains are more than depreciation deductions,

- capital gains are less than depreciation deductions, or

- there’s a loss.

When Selling with Capital Gains More than Depreciation Deductions

Per the previous example, you’re holding rental property bought 10 years ago for $390,000. Being 39-year property, you’ve written off $100,000 ($10,000 yearly) in depreciation deductions. With an adjusted $290,000 tax basis, it’s sold for $490,000 for a realized $200,000 capital gain.

You’ll pay up to 25% (based on ordinary income tax rate capped at 25%) on the part that’s tied to depreciation deductions. That’s $25,000 in depreciation recapture tax ($100,000 times 25%).

The remaining $100,000 will receive more favorable long-term capital gains tax treatment. Assuming you’re in the 20% top bracket, that would be $20,000 in capital gains taxes. Taxes would total $45,000 for a 22.5% effective tax rate.

When Selling with Capital Gains Less than Depreciation Deductions

Depreciation recapture applies to the lesser of the gain or your accumulated depreciation deduction. In the previous example, if you sell the property for $300,000, you’ll have a gain of $10,000 ($290,000 adjusted cost basis minus $300,000).

Less than the depreciation deductions, the gain is taxed at ordinary income tax rates capped at 25%. In this example, $10,000 times 25% for $2,500 in tax.

When Selling with a Capital Gains Loss

Depreciation recapture will not apply on losses. Say you sell for $190,000 in the previous example. You would report a loss of $100,000 ($290,000 adjusted cost basis minus the $190,000 sale price). While this is a big loss, you did benefit from $100,000 in depreciation expensed over the past 10 years. It could be considered a wash in that regard.

Except, the $100,000 is considered a §1231 loss. This means it can be used –

- to reduce your tax liability during the current tax year,

- as a carried-back offsetting income from the previous two years, or

- carried forward to offset future income.

A §1231 loss–not applied against a net §1231 gain–is an unrecaptured loss. These losses will be applied against net §1231 gain beginning with the earliest loss in the 5-year period.

The Impact of the Date of Placing the Property in Service

When the property was placed in service impacts §1250 depreciation recapture gain amounts.

Caution: there may be exceptions to the following general rules. You’ll likely want to seek professional guidance when selling long-held properties.

Contact either a certified CPA or one of the best 1031 exchange companies near you to get advice from their tax attorney specializing in 1031 exchanges. (We also have a guide about QIs: What Do 1031 Exchange Accommodators aka Facilitators aka Qualified Intermediaries Do for You?)

Property Placed in Service After 1986

All depreciation deductions accumulated before the real estate is sold constitutes unrecaptured §1250 gain. In the previous example–of the $200,000 gain–$100,000 represents unrecaptured §1250 gain that’ll top out at 25%. The remaining $100,000 portion of the gain maxes out at 20%.

Property placed in service between 1981 and 1986

For these years treatment depends on whether the real estate is residential or non-residential.

Residential real estate: Using straight-line depreciation, the above post-1986 rules apply. However, using a declining balance method, the gain is generally taxed in the following manner.

- Depreciation exceeding that allowable under straight-line depreciation is recaptured as ordinary income taxable up to 37% for tax year 2022.

- That portion of the gain not recaptured as ordinary income is taxed at ordinary income tax rates but capped at 25%.

- The remaining gain is capped at a 20% tax rate.

Non-residential real estate: Again, using straight-line depreciation, the above post-1986 rules apply. Using a declining-balance method, gains are taxed under these rules.

- Gains on allowable depreciation amounts are again recaptured at ordinary income rates maxing out at 37%.

- The remaining portion of the gain is capped at a 20% tax rate.

Pre-1981 Property

For real estate placed in service before 1981, the following rules generally apply.

- Again, depreciation amounts claimed above straight-line are recaptured as ordinary income capped at the top 37% tax rate.

- Any allowable depreciation balance remaining as unrecaptured §1250 gain caps out a 25% tax rate.

- Still any remaining gain caps out at a 20% tax rate.

Yes, more complications but here’s a quick review. Unrecaptured §1250 gain is part of the capital gain on real estate property sales. It’s that amount already depreciated. Previously depreciated, a higher capital gain rate applies capped at 25%. It only applies to depreciable real estate such as commercial and residential rental properties.

It should be apparent by now that real property tax laws are complex. Unless you’re a real estate tax pro, you’ll need professional assistance to avoid costly errors on selling these properties.

Does a 1031 Exchange Defer Depreciation Recapture Indefinitely?

Depreciation recapture and commercial property capital gains tax deferrals go together. With your first successful 1031 Exchange, you defer these taxes, effectively creating that IRS I Owe You (IOU). Any subsequent exchanges–there’s no limit–supplement it.

Not only a great wealth builder for investors, property that’s never sold can perpetuate pre-tax dollars.

Who Says the Only Two Things Certain in Life Are Death and Taxes?

On death while still holding tax-deferred properties, heirs inherit them with a stepped-up basis. This basis is the property’s fair market value at the time of death. Any deferred tax balances are eliminated. Capital gains and depreciation recapture tax IOUs are erased.[1]

Alert: Adding family member(s) to property titles–thereby gifting that property–voids their step-up in cost basis. To preserve that basis after the investors’ death, investment properties must pass directly to their heirs.

Back to that example: at death an investor owned investment property now with a $490,000 fair market value. Despite the family effectively realizing a $200,000 gain, none will be recognized. Heirs’ step-up cost basis is the same $490,000 FMV on receipt.

Sold immediately, there’s no gain on which to impose any taxes. Sold later absent an 1031 Exchange for $585,000, e.g. capital gains and depreciation recapture taxes apply to the $120,000 gain ($585,000 minus $465,000 cost basis).[2] Depreciation to be recapture is the amount expensed annually in total, say $25,000 over two full years ($490,000 ÷ 39-year property times 2 years).

See When selling with capital gains more than depreciation deductions above. Depreciation recapture applies to the $25,000 topping out at 25%. The remaining $95,000 of the $120,000 gain tops at a 20% tax rate.

Yet, heirs have the option to defer capital gains taxes again. They can complete 1031 Exchanges, replacing inherited properties with like-kind ones into perpetuity.

Known as Swap ‘till you drop, it’s a common refrain in the real estate investor world. It can be a call for investors to consider leaving heirs with investments capable of accelerating future wealth-building. Accomplished with investor savvy, 1031 Exchanges enjoy high success rates.

[1] Estate taxes could be imposed. Currently, the federal estate tax exemption is $11,580,000 per person. An exemption cutback into the $5,000,000 to $6,000,000 range per person is scheduled for 2026. Amounts exceeding the exemption are currently taxed at a 35% rate.

[2] Again for illustration, cost adjustments to selling and purchase amounts are disregarded.

How to Report 1031 Exchange Activities to the IRS

With a successful 1031 Exchange deferring all taxes, there’s no statutory requirement to file at all. You may wish to file nonetheless if only to start the statute of limitations running. Once the statute has run, any future IRS audit clawbacks are precluded. A short explanation can be attached to Schedule D or Form 4797 as applicable.

Form 4797 is used to report a business property sale. Business owners file Schedule D to report mergers or acquisitions. Both forms may be required depending upon the nature of actions taken during the year.

In either case, taxable boot whether cash or mortgage is reported on line 15 of Form 8824 Like-Kind Exchanges. Taxable income is subject to ordinary income tax rates. Depreciation recapture amounts are reported on line 21 of Form 8824 and line 16 of Form 4797 Sales of Business Property.

How to Ensure Your Exchange Is Legal and Safe?

Unless you are conducting a simultaneous exchange that doesn’t involve boot, you must use services of a Qualified Intermediary.

A professional, competent, and experienced 1031 exchange company with income tax experts on the team will advise you on the options you have to minimize your boot while getting the most of your relinquished property value.

They will ensure that the procedure is completed legally, in compliance with all IRS rules.

PropertyCashin is an all-in-one platform for commercial real estate investors that maintains relationships with top-rated 1031 exchange firms in all locations of the USA. To get connected with the best professionals and have your exchange processed safely and effectively, fill out the form below.