Commercial Property Tax Reduction Methods

**The information on this web page is provided for informational purposes only and should not be considered as legal, tax, financial or investment advice. Since each individual’s situation is unique, a qualified professional should be consulted before making financial decisions.**

From this guide you will learn about 5 effective methods that professional commercial property tax consultants use to reduce their clients’ commercial real estate property tax:

- commercial property tax deductions

- avoiding installment payment fees

- getting advantage of early payment benefits

- cost segregation studies

- property tax appeals

Note: to learn how commercial real estate tax is determined, read our other guide ABC’s of Commercial Real Estate Property Taxation in the USA. We also have comprehensive guides on the Federal Capital Gains Tax implications of selling commercial property and 9 ways of avoiding the capital gains tax on the sale of commercial real estate.

Now, let’s start with the most common method of reducing your commercial real estate tax.

How to Reduce Commercial Property Tax in the U.S.

1. Commercial Property Tax Deductions

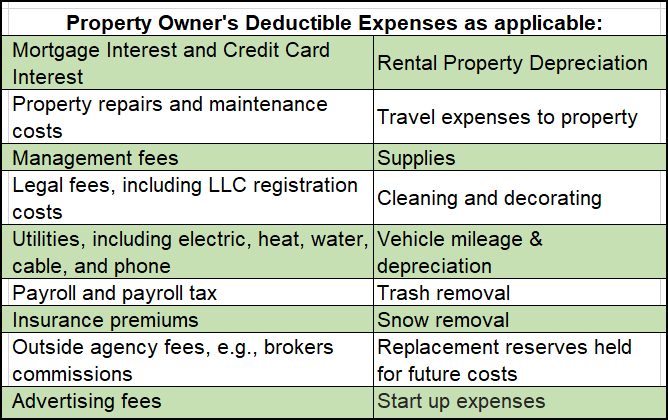

Regarding the potential deduction charted below, three issues deserve special attention.

1. Depreciation – Commercial rental property depreciates over 39 years per the IRS. On a $500,000 property, the annual depreciation expense is a mere $12,821 ($500,000 divided by 39 years). A Cost Segregation Studies, accelerated depreciation option, is covered in a later section.

2. IRS rules now allow nonresidential properties, i.e., commercial rental properties to take Section 179 deductions. The Tax Cuts and Jobs Act increases to $1,000,000 the maximum amount that may be expended and increases the phaseout threshold from $2M to $2,500,000.

It also expanded the definition of qualified real property to include improvements to nonresidential real property such as replaced roofs, heating and air-conditioning, security systems. This chart lists many potential deductions.

3. A prorated owner-occupied rental property tax deduction may be taken against your rental income. It’s treated as a separate investment property.

2. Avoid Installment Payment Fees

Be wary of extra charges associated with paying your real estate taxes quarterly. At the same time, many municipalities instead give discounts on installments (this is covered in the next section). Unless early payment benefits outweigh such fees, holding onto cash until payments are due seem prudent.

3. Early Payment Benefits

Little outweighs timing in importance when planning, whatever the tax! Taxation on commercial property in some states covers two years with one payment due each year. Both installments may be paid in the first year and deducted in the year paid. It’ll be a first-year tax reduction – next year tax increase.

Here are some timing factors that may cause you to pay early:

- With more taxable income expected this year than next, prepaying will keep you out a higher tax bracket both years.

- Prepaying will forestall an Alternative Minimum Tax (ATM) imposition that would preclude deductions such as property tax write-offs.

- Even better, a few jurisdictions discount early payments. Free money unless the benefits of postponing payment to the next year outweigh the discount.

Regarding discounts, just to list a few examples, California’s Orange County and Florida’s Pinellas County grant the same graduated 4% November to 1% February discount on payments due the end of March. Hillsborough County Florida offers a 4% discount on payments made by November 30. Okaloosa County Florida offers a 3.375% discount on its installment plan.

4. Cost Segregation Studies

Most real estate property has a 39-year tax recovery period while personal property is depreciated over 5 or 7 years. Cost segregation studies identify properties for reclassification from long- to shorter-life MACRS (Modified Accelerated Cost Recovery System) depreciation.

The concept is simple but not the process. Identifying qualified property is often left to engineering-based cost segregation firms. Commercial real estate owners may significantly increase their cash flow by identifying and reclassifying building assets (purchased or constructed since 1987) for faster depreciation. MACRS may be applied to non-structural building subcomponents such as office furniture, automobiles, computers, and the like.

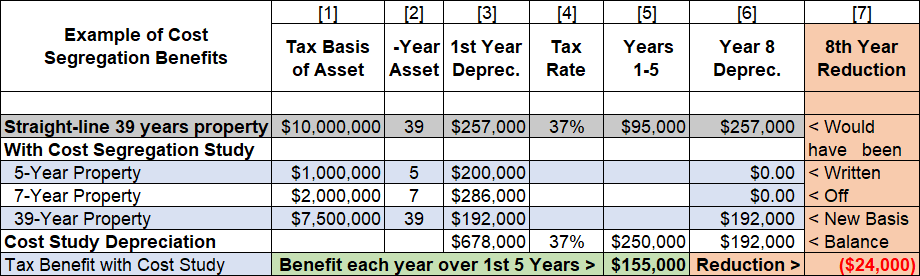

To summarize the example charted below:

- Column [5] With 39-year straight-line, each year’s depreciation would reduce tax due by $95,000 (37% tax rate times $257,000 depreciation).

- Column [5] Accelerated MACRS depreciation on study-identified subcomponents – coupled with remaining 39-year depreciation – produced $678,000 in depreciation and $250,000 in reduced taxes. That’s $420,000 more depreciation than going all straight-line, a $155,000 tax reduction for the next five year barring any adjustments.

- When the 5-year property is written off, tax savings go down a bit.

- Column [6] After year 7, all MACRS subcomponents have been written off. How tables are turned with depreciation at $192,000, which is $65,000 below what straight-line would have been on the full $10M tax basis that year.

- Column [7] With nothing changing – having written off 5- and 7-year property – $24,000 more in tax ($65,000 X 37% tax rate) would be paid over the next 32 years. Even so, these tax increases won’t catch up with early

Factors such as the present value of money along with opportunities to compound those early savings, makes it attractive if enough subcomponents are identified. According to Engineered Tax Services 20-30% of a building typically qualifies (even such items as light fixtures). One risk nonetheless is that subcomponents are few in relation to study costs.

There’s a Catch-up Depreciation potential, as well. What if you’ve owned property for several years? A cost segregation study could retroactively apply accelerated depreciation to the back-years. Even greater deductions may be possible with depreciation catch-up realized in the current year.

5. Property Tax Appeals

When should you be thinking about a closer look and possible assessment protest?

- There are obvious errors, such as incorrect property age or square footage.

- The assessment has spiked unexpectedly.

- Similar area properties have lower appraisals.

- Over years, no one has ever questioned a seemingly high assessment.

- Income is down.

- Operating expenses are up.

- Area vacancies are up.

Some things to know about commercial real estate tax appeals:

To get a sense of what’s involved, study a protest form such as Bucks County’s here.

Notwithstanding going-it-alone could be a long, complicated process, consider asking the assessor office for clarifications both as to the assessment’s basis and appeal procedures. If updating inaccurate data resolves everything, e.g., there may be no need for outside help.

However, if it’s a complex issue – such as challenging a cap rate (discussed earlier) – retaining counsel may be advisable. If it’s a high-dollar matter potentially destined for court, be aware some jurisdictions require licensed attorneys represent taxpayers. More about seeking professional help in the next section.

After getting the facts and learning the rules, you or your advisor must know what went into calculating your tax bill. Focus on the approach used to set the assessed value. Review the three common scenarios described earlier. They play key roles in calculating Assessed Value. Comb through the details for inaccuracy and misrepresentations.

Analyze how well the assessor’s calculation followed prescribed guidelines. Again, you or your advisor must know how it all works in that municipality. Facts and circumstances are your best offense. With a little luck, you might discover and have assets removed that were disposed of long ago.

Much beyond that, you’ll be asked to prove your property’s assessment is too high for current market values or it’s not consistent with the surrounding community. That’s likely to get sticky, potentially bordering on subjectivity.

You might challenge the assessor’s use of ill-suited one-size-fits-all conventions. Or if the assessor used an income approach, you might argue a shuttered anchor store nearby has depressed business. As a result, your NOI has tanked.

Both cases require specialized knowledge that you, staff, or outside counsel will require. A word of caution here: stir sleeping dogs at some risk. Triggering a multi-year tax audit is a double-edged sword, potentially creating a wave of refunds or alas deficiency assessments.

Then, if you or your advisor’s efforts produce no resolution, it’s on to a formal appeals process. Jurisdictions’ protocols vary and must be adhered to faithfully to avoid having your case go unheard. Haven’t yet engaged professional help? Now may be the time.

More to think about: making good on favorable hearing and court rulings. You win! Now how to ensure the proper and timely delivery on court order refunds, et al. It may require constant monitoring and taking steps to complete and verify compliance.

Amounts to be refunded, e.g., may require complex recalculations post-hearing. Then too, prodding the assessor’s office to conclude things in full compliance may become necessary.

Still undecided about retaining a consultant? Read on.

Hiring a Commercial Property Tax Consultant

With a little homework – much of it described in this article – you are in a good position to evaluate consultation needs and options. Take a comprehensive view, not just focusing on the protest itself!

Could you use help from the ground up, perhaps a professional appraiser for uncovering overvalued properties, computing capitalization (Cap) rates, or evaluating a Cost Segregation Studies potential for property? Or is all that well in hand and all you need is a court-required licensed attorney?

In the latter instance, it’s a question of retaining an attorney well-suited for the particulars of your case, able to hit the ground running – as a proven expert – with what you’ve put together. Cost is a question of general competence and competitive rate checking.

Otherwise, with cradle to grave help needs, return on investment (ROI) analysis may be in order. If that Study or other tax planning has real savings or earns potential, retaining a full-service firm might make sense.

They might handle both your appeal and – with lessons learned – complete an audit of your tax possesses at a bargain rate. You’ll not have to conduct the same due diligence all over again with a second consultant, as well.

There are also boilerplate recommendations for the selection process.

- Look for experience that fits your appeal whether it’s taxation on commercial or industrial property.

- Consider factoring in continued consultation post-appeal.

- Confirm the consultant is registered with the municipality hearing your appeal.

- Seek reliable, informed references that have first-hand experience with the firm.

- Check with the Better Business Bureau.

- Verify accuracy of solicitation letter data being used to projected appeal outcomes.

- With no ambiguity, confirm flat or contingency fees while avoiding variable fees. Contingency fees provide incentives to protest – if confident of winning – and compensation is proportionate to the reduction in assessed value they achieve.

- Review terms of the agreement meticulously and leave no material issues unresolved.

- Decline any demands for upfront fees to analyze your appeal.

If you are interested in being connected with reputable property tax consultants in your area, fill out the form below. As a national all-in-one platform for commercial real estate investors, we manage relationships with the top-rated tax consulting and appeal companies in each U.S. state and Washington D.C. After receiving your request, we will review it and connect you with the best local specialist who can help you.